Enel, the Italian energy giant, is increasing its commitment to clean power for the coming years. The company has unveiled its new 2026–2028 Strategic Plan, which outlines a major expansion in renewable energy and grid investment.

Under the plan, Enel will invest €53 billion over three years. This marks a 23% increase compared with the previous strategy. Of this total, nearly €20 billion will go directly into renewable energy projects.

The renewable spending will support the addition of 15 gigawatts (GW) of new clean energy capacity by 2028. This expansion will bring Enel’s total installed renewable capacity to about 80 GW globally.

The plan reflects the company’s effort to grow clean energy while maintaining financial discipline. The company aims to strengthen earnings and improve returns, while accelerating the shift to low-carbon electricity.

Flavio Cattaneo, CEO of the Enel Group, said:

“Today, Enel presents an ambitious and credible Strategic Plan with a sharp acceleration in growth thanks to an increase of Greenfield and Brownfield investments, which will lead to further improvement of the Group’s risk/return profile. The managerial actions carried out in the last three years provide us with the financial flexibility to invest in the most dynamic markets in terms of electricity demand.”

€20 Billion Commitment: The Clean Power Blueprint

Under Enel’s 2026–2028 Strategic Plan:

- €20 billion will fund renewable energy projects.

- Enel will add 15 GW of new renewable capacity by 2028.

- Total renewable capacity will rise to about 80 GW.

- The company’s total gross investment across all businesses will reach €53 billion over three years.

- These figures show a strong push toward carbon-free power. Renewables now represent one of the largest components of Enel’s capital plan.

The new capacity will focus mainly on wind and solar power. These technologies remain cost-effective and scalable. Enel will also invest in hydroelectric plants and battery storage systems. These technologies help balance wind and solar output.

By adding 15 GW, Enel is positioning itself among the largest global renewable power producers.

How This Fits Into Enel’s Broader Strategy

The €53 billion investment plan covers more than renewables. A large share of spending will go to electricity networks, wherein grid modernization remains a key priority. Stronger grids allow more renewable energy to connect and flow efficiently.

The company is directing most investments toward markets in Europe and North America, which together account for more than €23 billion of total planned spending. Around €3 billion is allocated to Latin America.

Enel expects its strategy to generate solid financial results. Over the 2026–2028 period, the company projects cumulative ordinary EBITDA of €74 billion.

The company says it will maintain a disciplined approach to capital allocation. It plans to focus on projects with stable regulation, clear returns, and predictable cash flow.

Where the Renewables Will Grow

Enel’s renewable expansion will cover several key technologies, including:

-

Onshore Wind and Solar

Most of the 15 GW addition will come from onshore wind and solar farms. These projects can be built at scale and deployed quickly.

Wind and solar are central to Enel’s strategy because they deliver competitive electricity costs and support decarbonization goals.

-

Hydro and Dispatchable Renewables

Hydropower remains important for Enel. Unlike solar and wind, hydro can generate electricity on demand. This helps stabilize grids when renewable output varies.

Dispatchable renewable assets help ensure a steady supply during peak demand.

-

Battery Storage

Battery systems are essential for integrating variable renewables. Storage allows electricity to be saved and used later.

By combining wind, solar, hydro, and batteries, Enel aims to provide cleaner electricity around the clock.

From Coal Exit to Renewable Leadership

Renewables are central to Enel’s long-term climate goals. The company aims to achieve 100% renewable generation and fully exit coal by 2040. This objective aligns with global decarbonization targets and European climate policy.

Electricity demand continues to rise worldwide. Growth is driven by the electrification of transport, industry, and heating. Data centers and digital services also increase demand.

As more sectors shift from fossil fuels to electricity, utilities must expand clean generation capacity. Enel’s investment plan responds directly to this trend.

By scaling renewables and strengthening networks, the company aims to support both climate goals and rising electricity consumption.

What’s Inside Enel’s 2040 Net-Zero Goals?

Enel has set clear goals to fight climate change. The company aims to reach net zero greenhouse gas emissions by 2040, a full decade sooner than the global 2050 target set under the Paris Agreement. This means Enel plans to eliminate all direct and indirect emissions across its operations and value chain.

A key part of this strategy is switching all energy production to sustainable sources like wind, solar, and hydroelectric power. Enel also plans to exit the natural gas sector, so renewable electricity will be the only type of energy it supplies to its customers.

Enel’s climate targets align with the 1.5°C limit — the most ambitious goal of the Paris Agreement. These targets have been validated by the Science-Based Targets initiative (SBTi), meaning they follow science-based methods for emissions reduction.

The company has outlined milestone steps on the path to 2040. By 2025, it expects renewables to make up about 75% of its total electricity production. By 2027, Enel plans to finish phasing out all coal-fired power plants. Then by 2040, all of its installed capacity will come from renewable sources, and all direct and indirect emissions will be eliminated.

Enel has already made measurable progress. Its operational emissions (Scope 1 and Scope 2) have dropped significantly from a 2017 baseline. The company is working to reduce emissions across its value chain (Scope 3 emissions) as well.

To support these goals, Enel engages with suppliers and customers. It helps them reduce their own emissions through clean energy solutions and energy efficiency programs. This broader approach aims to cut emissions not just within Enel’s operations, but across the entire energy ecosystem.

Scaling Renewables Amid Market Pressures

The energy sector faces ongoing challenges. Rising interest rates have increased financing costs. Supply chain issues have affected equipment delivery. Inflation has pushed up construction expenses.

Enel acknowledges these pressures. The company says it will prioritize projects that offer stable returns and operate in strong regulatory environments.

Partnerships and flexible financing will also help manage risk. This includes cooperation with institutional investors and local partners.

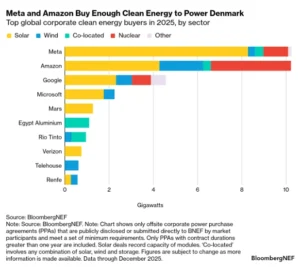

Despite these market challenges, the long-term outlook for renewables remains positive. Clean energy continues to attract capital as governments and businesses pursue decarbonization. Big tech companies are the major purchasers of clean energy, with booming data centers as the main driver.

Utilities Powering the Next Phase of Decarbonization

Enel’s decision to invest €20 billion in renewables and €53 billion overall through 2028 signals confidence in clean energy as a core growth driver.

The planned 15 GW capacity increase will strengthen its position as a major renewable producer. It will also support grid stability and energy security in key markets.

As countries set ambitious 2030 and 2040 climate targets, utilities like Enel play a central role. Expanding renewable capacity, modernizing grids, and maintaining financial discipline are all essential parts of the transition.

Through its 2026–2028 plan, Enel aims to balance sustainability with profitability. By scaling renewables while maintaining strong earnings, the company is positioning itself for the next stage of global energy transformation.